Covid-19 brought the world to a grinding halt, and the associated business closures triggered a deep economic downturn. To limit the economic damage, governments and central banks across the globe provided massive economic and monetary stimulus, which helped the limping economies to regain lost strength. On the flip side, over the last 12 months, inflation has seen a massive uptick, e.g. In February 2022, CPI in the US surged to 7.9% Y-o-Y. It is the highest level seen in the last 40 years. Due to pent-up demand and supply chain disruptions, it has been on the boil.

The Fed has two jobs: keeping inflation under check and maximising employment. While unemployment is declining, inflation has been running red hot. Earlier, the Fed opined that the inflation was ‘transitory’ in nature; however, in the January 2022 FOMC meeting, they acknowledged that it is not ‘transitory’. Rising inflation combined with falling unemployment and strong growth has prompted the Fed to reduce the money supply and consider aggressive rate hikes.

For a long time, the fed fund rate was held close to zero, and this would be Fed’s first rate hike since 2018. Markets experts anticipate 5-7 rate hikes of 25bps each in 2022 alone. As a result, many investors have been worried that the rate hike would trigger a fall in stock prices.

It is a commonly held belief that interest rates and stock prices move in the opposite direction. In theory, it makes sense as the stock prices reflect the future earnings discounted to present value using the interest rate. Therefore, higher interest means that the future earnings would be worth less today and vice versa.

Most investors would be convinced of the same, as in the last two decades (2000-2020), they have witnessed three bull runs post rate cuts. Firstly in the backdrop of the dot com bubble (1999-2001), the rate cut fueled a bull run up to 2008. Then, once again, post the Global financial crisis (2008), the fed reduced the interest rate close to zero, and the investors witnessed one of the largest and longest bull markets. And even very recently, post-Covid crisis investors witnessed a strong bull run.

Does this mean the US stock market’s poster boy- the S&P 500 would take a beating once the Fed goes in for rate hikes?

Although historically, rate cuts during recessions have resulted in strong bull markets, e.g. Covid crisis and Global Financial Crisis, but does this work the other way round?

The same cannot be said during rate-hike cycles.

In 2020, humanity witnessed a global pandemic of a scale that was never seen before. But what impact does it gave to healthcare mutual fund investments? Find out more on the impacts of Covid 19 on investment; on next blog.

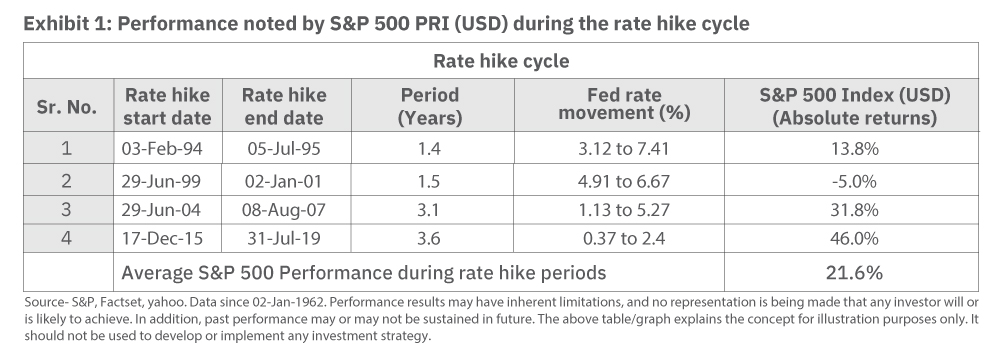

Turning a few pages into history will assure you that rate hikes alone aren’t bad for stocks.

As shown above, over the last ~30 years, there have been four rate hike cycles. On average, the S&P 500 has returned 21.6% on an absolute basis. One exception was the rate hike cycle during 1999-2001; the S&P 500 noted negative returns as the rate hike coincided with the Dotcom crash.

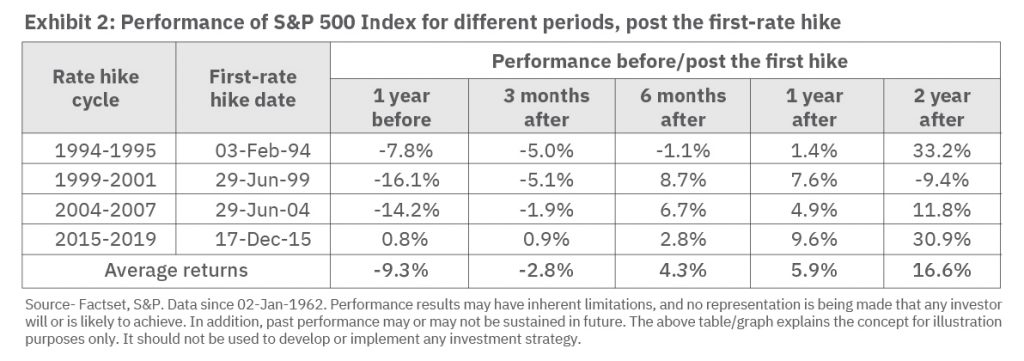

Let us analyse How the index performs during the rate hike starting from the first-rate increase to strengthen our conviction.

As shown in Exhibit 2 above, the first few months after the first rate hike, the S&P 500 noted higher volatility. For example, it was down by 3% (avg return) at the end of three months from the first hike; however, it noted positive average returns for all subsequent periods mentioned above. To say the least, the data seems to be surprising, but generally, rate hikes are preceded by solid economic growth and higher inflation. Therefore, a balance of economic growth and inflation is considered conducive to stock markets.

While taking a leaf out of history helps investors analyse an event rationally, it is equally important to acknowledge the ever-evolving macro-economic environment and the challenges it may throw.

Co-author: Mahavir Kaswa, Head of Research, Passive funds, Motilal Oswal, AMC

This article was also published on the digital platform zeebiz.com; reference: https://bit.ly/3JwtGj3

Disclaimer:This article has been issued based on internal data, publicly available information and other sources believed to be reliable. The information contained in this document is for general purposes only and not a complete disclosure of every material fact. The information/data alone is insufficient and shouldn’t be used to develop or implement an investment strategy. It should not be construed as investment advice to any party. All opinions, figures, estimates and data included in this article are as of date. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The statements contained herein may include statements of future expectations and other forward-looking statements based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible/liable for any decision based on this article. Mutual Fund investments are subject to market risks; read all scheme related documents carefully.