Neeraj Chopra become a household name after he won a gold medal in Javelin throw at the Tokyo Olympics in 2021. Javelin throw is a sport of throwing a spear at the farthest possible distance. The athlete does so by first running a small distance to gain motion which helps them throw the javelin as far as possible. Similarly in Space exploration, the spacecraft initially circles the earth for several days to gain enough motion before exiting the atmosphere.

Noticed anything common between the two? In both cases, a lot of initial motion was built up to get the desired result. Such motion can be referred to as momentum & can be applied everywhere from the surface to space. As momentum has varied applications across science and sports, it can also be applied in investing.

Application of “Momentum” in Investing

Momentum investing is a strategy that invests in securities that have momentum (usually upward trending prices) and looks to sell them once they lose momentum. It works under the hypothesis that markets will continue to move in a particular direction for a much longer period than most people assume is possible. It implies that well-performing securities will continue to do so & vice versa.

The momentum for a security is decided basis the price trend. Since all decisions revolve around price, for momentum, ‘Price is the almighty’ or popularly known as ‘Bhaav bhagwaan che’.

“The premier market anomaly is momentum. Stocks with low returns over the past year tend to have low returns for the next few months, and stocks with high past returns tend to have high future returns.”

– Eugene Fama and Ken French (fathers of Efficient Market Hypotheses)

Does momentum work?

Is the momentum strategy bang for the buck? A good starting point will be to look at the historical performance & the consistency of the returns. In Exhibit 1, we can see that momentum has outperformed broad-based equity across different periods. In longer-term periods, the out performance is particularly significant as it went as high as ~7% in the last 10 years.

Momentum = Nifty200 Momentum 30 TRI

Equity Markets = Nifty 200 TRI

Disclaimer: niftyindices; total returns index (TRI) used for performance calculations as of close of 31-May-07 to 31-May-22. Past performance may or may not be sustained in future.

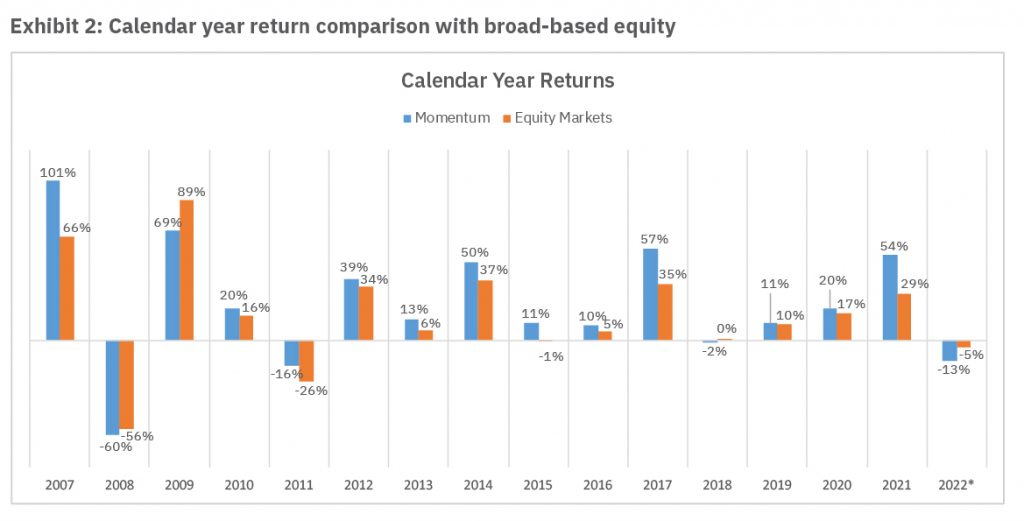

Momentum = Nifty200 Momentum 30 TRI

Equity Markets = Nifty 200 TRI

Disclaimer: niftyindices; total returns index (TRI) used for performance calculations as of close of 31-Dec-06 to 31-May-22. *2022 Year To Date (YTD). Past performance may or may not be sustained in future.

As shown in Exhibit 2, the momentum strategy has outperformed the broad-based Nifty 200 index in 12 out of the last 16 years. Both the exhibits clearly show that the strategy has worked historically in the Indian markets & investors should have a look at it.

Why does momentum work?

Momentum works mainly because it tries to take advantage of emotional (behavioural) mistakes made by investors like fear, greed, overconfidence, etc. The other possible explanation might be irrational human behaviour that arises due to several behavioural biases. Such behavioural biases are difficult to avoid as they influence our decision-making process unconsciously.

Some biases that we might experience on a daily bases include:

- Confirmation bias: When investors like a particular stock, they generally tend to only look at facts that support their narrative & ignore other data. This causes confirmation bias among investors which might lead them to incorrect decision making.

- Overconfidence bias: Investors in bull markets generally make quick profits & may confuse luck with skill. This leads to the tendency of overestimating the extent of their abilities compared to actual skills & thus making inferior choices.

Momentum tries to capture such human errors as it opens up the opportunity for security mispricing in the market.

Disclaimer: The image mentioned above are used to explain the concept and is for illustration purpose only and should not be used for development or implementation of any investment strategy. It should not be construed as investment advice to any party.

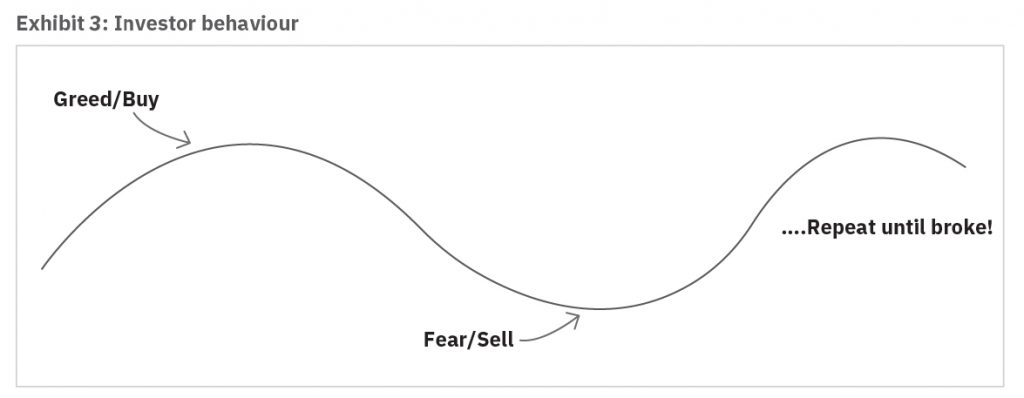

As is evident from exhibit 3, investors are always trapped in the endless cycle of fear & greed. When stocks have rallied too much, investors have the fear of missing out as they tend to see other investors profiting from the rally. But when the market has corrected or fallen by a huge margin, panic takes over which leads to investors selling their holdings. Hence, momentum will continue to take advantage of such mispricing as long as investors will make errors in their judgement.

Is it the perfect strategy then?

Momentum is not perfect & does have its limitations. As the strategy picks up securities with the highest motion/momentum, historically it is observed that such strategies experience higher volatility. Further, such strategies fall more during market corrections (downtrend) compared to broad-based equity. Since this is a trend based strategy, it has to strictly follow market movements which results in higher portfolio churn. The best way to address these is to invest with a fairly long term investment horizon.

To conclude, momentum has performed well in the past & may continue to do so as long as it can take advantage of the mispricing in the market. Studies show that it has worked across various markets & in India, it is becoming increasingly popular among investors. Such a strategy is best suited for a long term investor. Considering the risks, momentum has the potential to highly reward its investors if they are in for the full ride.

This article was covered by The Economic Times’ on 23th June 2022

Disclaimer: This article has been issued on the basis of internal data, publicly available information and other sources believed to be reliable. The information contained in this document is for general purposes only and not a complete disclosure of every material fact. The information / data herein alone is not sufficient and shouldn’t be used for the development or implementation of any investment strategy. It should not be construed as an investment advice to any party. All opinions, figures, estimates and data included in this article are as on date. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible/liable for any decision taken on the basis of this article. Investments in securities markets are subject to market risks, read all the relevant documents carefully.