Dear Investors & Partners,

Happy New Year to you and your family!

Life takes one more step forward as we usher in the year 2022. The year 2021 witnessed a transition from the complete lockdown restrictions imposed in the global economy, markets and our everyday life in 2020. True to being transitory, though 2021 brought hopes and signs of revival in business activity and economic momentum, it was plagued with its own set of problems. The mayhem caused by different Covid-19 variants along with supply chain bottlenecks deeply afflicted human lives and business activities.

Unprecedented monetary and fiscal support globally as well as in India to tackle the crisis created a situation of excess liquidity, which induced a strong rally in global assets. Equities, especially, continued to gain momentum. Another encouraging trend that evolved over 2021-22 was the advent of retail investors as the most potent force in equity markets both globally and in India.

Excess global liquidity, signs of corporate earnings recovery, low interest rate regime and a strong participation by retail investors enabled the markets to reasonably withstand persistent FII selling in 4Q21, amid all the Covid-related headwinds.

Actively managed equity funds came back with a vengeance and added strong alpha during the year. The Large Cap, Mid Cap, Small Cap and Flexi Cap categories delivered strong returns of 26.54%, 44.94%, 63.04%, and 32.08%, respectively. The Nifty-50 and Nifty-500 delivered 24.12% and 30.19% returns, respectively. Underpinned by strong returns, the share of equity-oriented schemes shot up to 48.0% of the industry assets in Nov’21 from 39.7% in Nov’20.

“In the midst of chaos, there is also opportunity” ― Sun Tzu

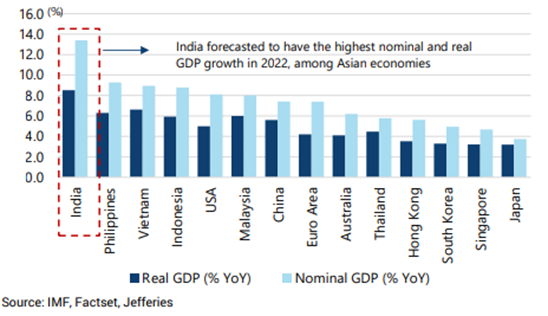

We believe India has entered into a phase of cyclical upturn and may witness a repeat of the economic upcycle similar to 2003-2010, with the fastest GDP growth among Asian countries.

As global population moves towards the herd immunity led by vaccinations and the Omicron variant, we may see the pandemic being transformed into an endemic over the next few months. As markets open up and Covid-induced bottlenecks ebb, we expect a revival in both demand and exports. With supply bottlenecks also alleviating steadily, India is well poised to truly capitalize on the China+1 opportunity.

Cleaner and well-capitalized bank balance sheets, deleveraged corporate balance sheets, a long-lasting revival in housing sector and a growth supportive monetary policy offer a prime setup for a durable economic and corporate earnings upcycle. The government’s recent initiatives on PLI and earlier corporate tax reforms have already laid the ground for it. We anticipate the government to support growth further in the upcoming Union Budget 2022.

Buoyed by the economic upcycle, return on equity for listed companies may hit the 12.5% mark in FY22 – the highest in last seven years. We also expect an uptick in corporate risk appetite for private capacity expansion by the year end.

However, likely rise in interest rates and a decline in market liquidity in FY22 may raise some eyebrows on company valuations. Increasing interest rates with moderate rise in inflation, albeit, could be great for capital formation, commodities and financial companies.

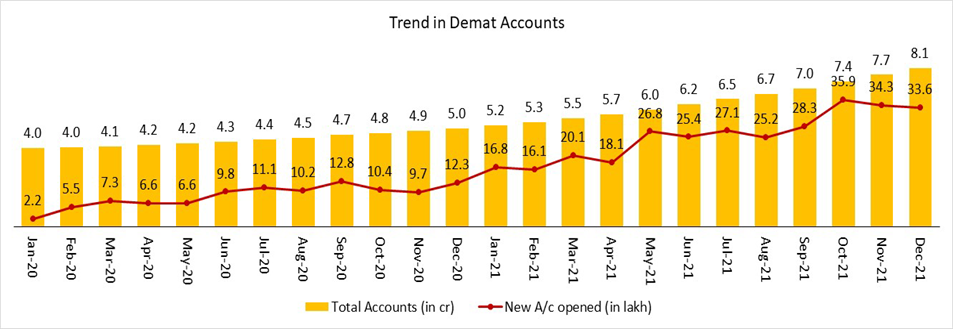

On the market front, retail participation will continue to gain in strength. Who could have in one’s wildest dreams imagined that the number of demat accounts that took decades to cross the 3cr number in Mar-18 have now crossed the 8cr mark.

Having said that we believe 2022 will be the year of selectivity. Compared with the broad-based rally last year, we expect 2022 to be conducive for bottom-up focused stock selection. We are positive on Financials, Discretionary Consumption and Technology Sectors and expect them to outperform in 2022.

Large banks are very well placed on credit quality front. Such banks have cleaner balance sheets after provisioning, have seen strong gains in market share v/s their PSU and weaker private sector counterparts and are available at reasonable valuations in the context of improving credit growth and emerging asset quality cycle. We believe domestic insurance companies will offer a long runway of strong growth and prefer them over the consumer staples companies as structural bets on India’s doubling of GDP to USD 6bn in the coming decade from USD 3bn at present.

We are also bullish on the discretionary consumption segment due to its projected strong demand growth trend. A large portion of this growth is likely to come from release of pent-up demand backed by improved mobility, gradual lifting of restrictions, extended store open time, and greater penetration of modern trade. The beneficiaries would include autos, building material & home improvement, durables, etc.

Incremental impacts of economic growth and wealth accretion on lifestyles always reflect in a disproportionate, non-linear growth on discretionary spends. Within discretionary also similar trends reflect on the premium products/services in respective segments.

Digitization, which saw multiple IPOs of new age tech companies, is expected to remain one of the predominant themes playing into the next year also. Digitization has also benefited traditional Indian IT companies; helping them grow at a faster pace in several years.

As India moves forward towards the coveted mark of USD6tn economy, our flagship PMS strategy – Motilal Oswal Next Trillion Dollar Opportunity – is all set to capitalize on the wealth creation, which follows such a shift. The strategy is specifically targeted to capture the uptrend.

Our mutual fund offerings – especially our flagship fund Motilal Oswal Flexi Cap Fund and also Motilal Oswal Large and Midcap Funds – are poised for long-term growth opportunity. For investors seeking tax benefits along with a growth-oriented portfolio, Motilal Oswal Long Term Equity Fund combines both the objectives.

In sum, markets and portfolio management styles go through cycles similar to our everyday life. We expect markets to incrementally reward the focused style of investing with price sensitivity for companies that are poised to contribute in the upcoming economic revival. Our investment process QGLP (Quality, Growth, Longevity and Price) is expected to help us capture the upside in the most optimum way.

Look forward to our continued partnership in the journey of wealth creation!

“Source : Jefferies Report”

Disclaimer: This article has been issued on the basis of internal data, publicly available information and other sources believed to be reliable. The information contained in this document is for general purposes only and not a complete disclosure of every material fact. The information / data herein alone is not sufficient and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party. All opinions, figures, estimates and data included in this article are as on date. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible/liable for any decision taken on the basis of this article. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.